Executive Summary for Clients

As your realtor and advisor, I frame it this way: Rent is the price of someone else's security. A mortgage is the price of your own.

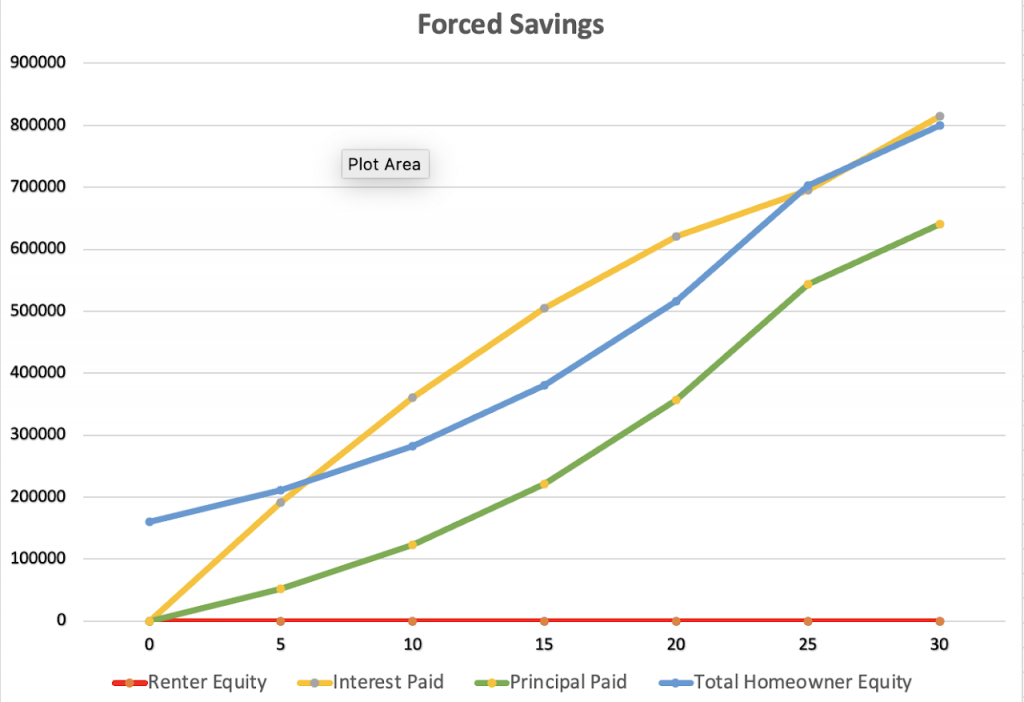

Even if the real estate market stays perfectly flat for 30 years, the homeowner ends up with a free-and-clear asset worth hundreds of thousands of dollars, while the renter is still subject to the "unrecoverable costs" of an ever-increasing rental market.

This Rent vs. Buy Analysis video breaks down the specific math of "unrecoverable costs," explaining why the hidden "burn rate" of renting often outweighs the maintenance costs of homeownership over a 5-to-10-year horizon.

Disclaimer : Projections are hypothetical models and do not guarantee future performance. Real estate values are subject to market volatility.