The Greater Sacramento region :

The Hidden Wealth Engine: Understanding the "Forced Savings" Effect

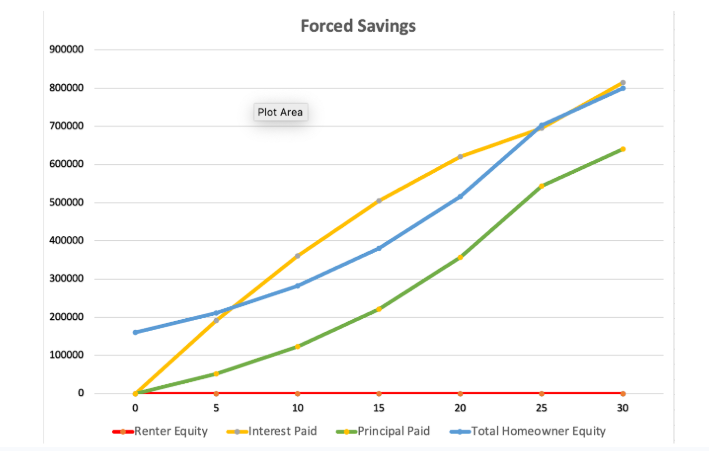

The "forced savings" effect is the most reliable, yet often overlooked, part of real estate. While a renter's entire payment is a sunk cost, every mortgage payment contains a principal paydown component that acts as a deposit into your own net-worth account.

The Forced Savings Mechanics

Even with 0% market appreciation, your wealth grows through the amortization schedule.

The Pivot Point: In the early years, the majority of your payment covers interest. However, as the balance drops, the interest charged decreases, and the principal paydown portion accelerates every month.

The Renter's Opportunity Cost: A renter paying $3,000 per month in a Bay Area suburb is effectively spending $36,000 per year without building equity.

Regional Case Studies: Principal Paydown at 0% Appreciation

Calculated using 2026 median values and a standard 30-year fixed mortgage.

1. Livermore Property (Tri-Valley Anchor)

- Purchase Price: $1,100,000

- Monthly Payment (Est.): $6,200 (P&I)

- Year 1 Principal Paydown: ~$12,500

- Year 10 Principal Paydown: ~$18,400

- 10-Year Cumulative Savings: ~$154,000

The Pop: In a zero-growth market, you have effectively accumulated more than $150,000 in equity while the renter in the same neighborhood has no comparable asset.

2. Sacramento Property (Highway 50 Corridor)

- Purchase Price: $550,000

- Monthly Payment (Est.): $3,100 (P&I)

- Year 1 Principal Paydown: ~$6,250

- Year 10 Principal Paydown: ~$9,200

- 10-Year Cumulative Savings: ~$77,000

The Pop: By Year 10, your monthly principal reduction is nearly 50% higher than it was during the first year of ownership due to mortgage amortization.